Sunoco (SUN)·Q4 2025 Earnings Summary

Sunoco Posts Transformational Q4 as Parkland Deal Boosts Revenue 63%—Stock Drops 7% After Hours

February 17, 2026 · by Fintool AI Agent

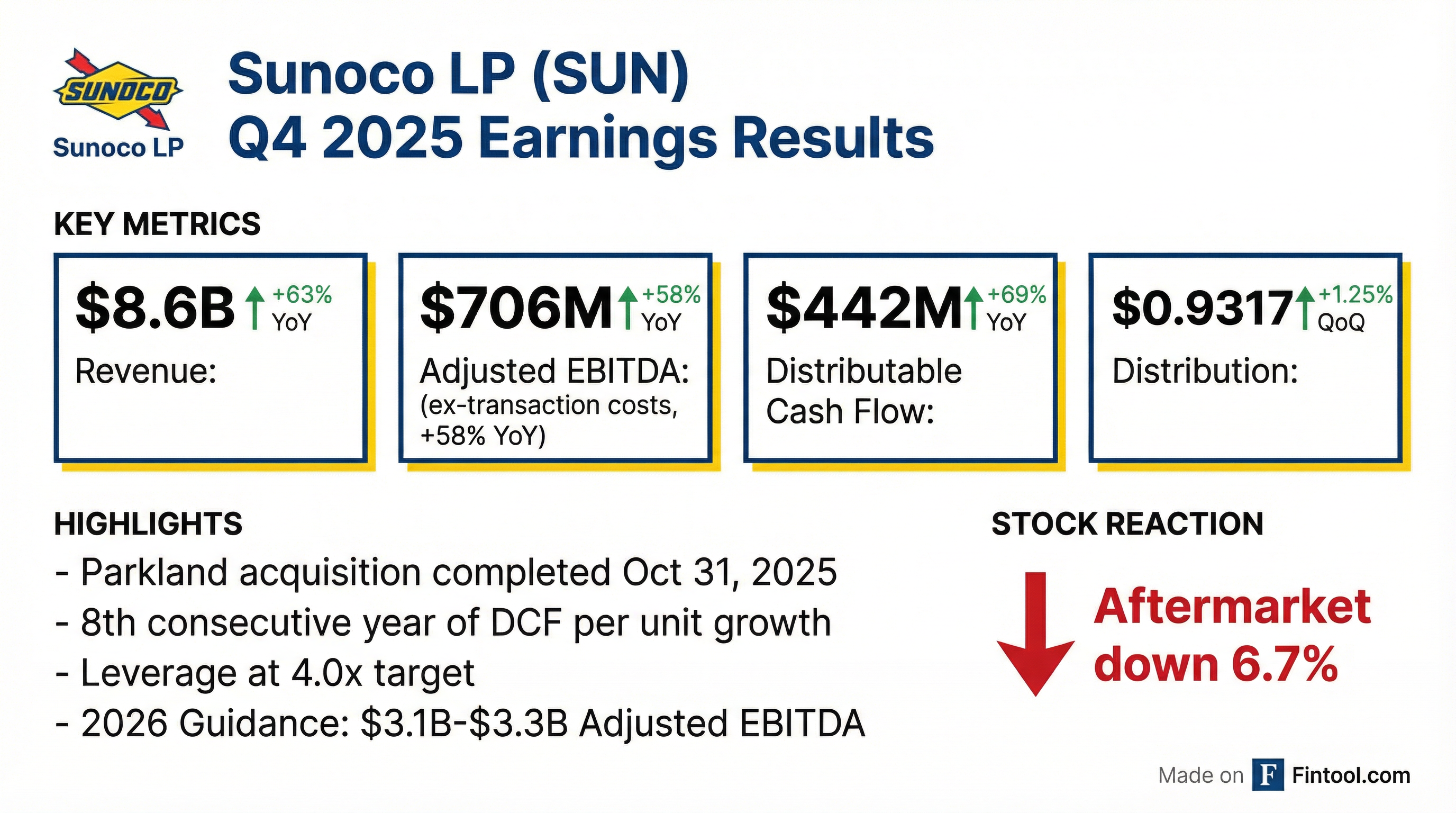

Sunoco LP delivered a transformational fourth quarter with the completion of its $2.6 billion Parkland Corporation acquisition, pushing revenue up 63% year-over-year to $8.6 billion and Adjusted EBITDA to a record $706 million excluding transaction costs . Despite beating expectations on key operating metrics, the stock fell 6.7% in after-hours trading as investors digested GAAP diluted EPS of just $0.09 versus $0.75 in the prior year, reflecting acquisition-related expenses.

On the earnings call, CEO Joe Kim emphasized Sunoco's unique positioning as "both a thoughtful defensive play as well as an attractive growth story," noting the partnership is now the largest independent fuel distributor in the Americas spanning 32 countries . The partnership announced its eighth consecutive year of distributable cash flow per unit growth and increased its quarterly distribution by 1.25% to $0.9317 per unit .

Did Sunoco Beat Earnings?

Yes, decisively on operating metrics. Adjusted EBITDA of $706 million (excluding $60 million in transaction-related expenses) significantly exceeded consensus expectations of approximately $491 million . Normalized EPS came in at $1.15 versus consensus of $0.96—a 19.7% beat.*

*Values retrieved from S&P Global

The revenue beat is largely attributable to the Parkland acquisition, which was not fully reflected in pre-deal consensus estimates. The partnership operated with only two months of Parkland contribution in Q4 .

How Did Each Segment Perform?

The Parkland acquisition dramatically reshaped Sunoco's business mix, adding a new Refinery segment and significantly expanding Fuel Distribution operations to 32 countries and territories .

Fuel Distribution sold 3.3 billion gallons at $0.177 per gallon margin—up from $0.107 last quarter—reflecting the higher-margin geographies in Parkland's portfolio . Legacy Sunoco volumes grew 2%+ versus prior year compared to flat U.S. demand . Pipeline Systems hit 1.4 million barrels per day throughput, with Q4 the strongest quarter of the year driven by agricultural markets . The new Refinery segment delivered improved performance versus prior years under Parkland ownership .

Geographic Deep Dive

Management provided extensive color on each region's contribution to the fuel distribution transformation:

U.S. (Foundation): Legacy volumes outperformed flat EIA demand trends by 2%+ thanks to growth capital deployment and roll-up M&A. Margin environment remains bullish with elevated breakevens.

Canada (Upside Surprise): "The closer we get to it, the more we like it." Canadian markets structurally resemble the U.S. West Coast and Northeast—high barriers to entry, regulated markets, elevated real estate and labor costs—all correlated with strong margins. Demand has been flat-to-slightly up versus the U.S. flat-to-slightly down trend.

Caribbean (Strong Momentum): Operations span 25 jurisdictions with onshore business in 22. Guyana exposure is particularly compelling with 20%+ GDP growth over three years, and Suriname is "up next" given offshore oil discoveries. Markets are either highly regulated (stabilizing margins) or open competition where Sunoco's scale provides "significant margin advantage."

How Did the Stock React?

Sunoco shares closed the regular session at $59.51, up 1.0% from the previous close. However, after the earnings release, the stock dropped 6.7% to $55.51 in after-hours trading.

The negative reaction likely reflects:

- GAAP EPS compression: Diluted EPS fell 88% to $0.09 from $0.75 YoY

- Transaction costs: $60 million in Q4 alone, $77 million for full-year 2025

- Net income decline: $97M vs $141M in Q4 2024 despite the acquisition

- Leverage concerns: Long-term debt ballooned to $13.4 billion from $7.5 billion

The stock has traded in a range of $47.98 to $60.62 over the past 52 weeks, currently sitting near the top of that range despite today's after-hours weakness.

What Did Management Guide?

Sunoco provided robust 2026 guidance in January, which remains intact. Key assumptions have already been validated:

The partnership noted a 50-day planned turnaround at Burnaby Refinery beginning in late January 2026 that will impact Q1 results . The TanQuid acquisition closed in January 2026, adding European terminal capacity .

What Changed From Last Quarter?

Management also introduced a new reporting format: SunocoCorp LLC (SUNC) now trades on NYSE, consolidating Sunoco LP into its financial statements. SUNC expects minimal corporate income taxes for at least five years, keeping distributions essentially equivalent to SUN LP distributions .

Q&A Highlights

On Margin Sustainability (Barclays): Analysts questioned whether the $0.177/gallon margin is sustainable. CCO Austin Harkness acknowledged there will be "quarter-to-quarter variability" but emphasized Sunoco doesn't "target or solve for a CPG number"—they optimize for fuel profit and sustained EBITDA growth. He noted Parkland brought more street margin exposure in geographies Sunoco "really likes."

On Synergy Confidence (RBC): Asked whether they could exceed synergy targets, COO Karl Fails was direct: "If you were deciding to take the over or the under, I would take the over on us delivering on our synergies." He noted integration activities started in Q4 and should exit 2026 "well north of $125 million on a run rate basis."

On M&A Pipeline (JPMorgan): CEO Joe Kim framed the $500 million bolt-on guidance as a "floor"—U.S. alone could absorb that amount given fragmentation, plus now they have Canada, Caribbean, and Europe as additional runways. "Best projects win," he said, noting they slowed down 2025 to focus on Parkland integration.

On Regulatory Tailwinds (Stifel): Asked about the EPA greenhouse gas endangerment finding rescission, Kim said while short-term impact is minimal, it's "bullish for refined products" longer term. Any legislation creating state-by-state specs adds complexity "that's always gonna be good for Sun... We thrive in those environments."

Key Management Quotes

On the acquisition: "NuStar was a home run acquisition, and Parkland's gonna be another home run acquisition for us." — Karl Fails, COO

On dual positioning: "We are uniquely positioned as both a thoughtful defensive play as well as an attractive growth story." — Joe Kim, CEO

On DCF track record: "Sunoco is the only AMZI constituent to grow DCF per common unit for each of the last eight years, and we expect this to continue." — Joe Kim, CEO

On Canada: "The Canadian business is gonna be an outstanding addition to our portfolio." — Austin Harkness, CCO

Capital Allocation & Balance Sheet

Sunoco ended 2025 at its long-term leverage target of approximately 4.0 times net debt to Adjusted EBITDA—achieved within 2-3 months versus the 12-18 month guidance post-Parkland close .

The $0.9317 per unit quarterly distribution ($3.73 annualized) represents the fifth consecutive quarterly increase and is consistent with the partnership's multi-year distribution growth strategy of at least 5% annually .

Key Risks to Monitor

- Integration execution: Realizing $125M in Parkland synergies while managing 32-country operations

- Leverage: $13.4B in debt despite hitting 4.0x target; rising rates could pressure coverage

- Refinery exposure: New Burnaby facility adds commodity margin volatility not present in prior business mix

- Currency risk: Parkland's Canadian dollar functional currency introduces FX exposure

- Distribution sustainability: Maintaining 5%+ growth with elevated debt service

Forward Catalysts

- Q1 2026 Earnings: First full quarter of Parkland integration (expected May 2026)

- Burnaby Turnaround Completion: 50-day maintenance ending ~March 2026

- TanQuid Integration: European terminal network expansion

- Synergy Realization: Progress toward $125M target through 2026

- Distribution Increases: Quarterly announcements targeting 5%+ annual growth

This analysis incorporates the Q4 2025 earnings call held at 9:00 AM CT on February 17, 2026. View the Q4 2025 earnings call transcript, 8-K filing, or prior quarter's earnings.